Filing a roof insurance claim in Lake Park, FL doesn’t have to be a stressful ordeal if you follow a clear, professional process. Whether your home is near Kelsey Park or closer to the Lake Park Harbor Marina, navigating the complexities of Florida insurance requires the right approach. Our latest 2026 guide walks you through the critical first steps, from performing a safe initial assessment to documenting every detail of the storm damage for your adjuster, ensuring a smooth roof insurance claim Lake Park FL.

When dealing with a roof insurance claim Lake Park FL, it’s essential to keep all communication documented and organized. This attention to detail will ensure that your claim process goes as smoothly as possible.

Quick Summary

Filing a roof insurance claim in Lake Park, FL requires prompt action and thorough documentation. Start by safely assessing the damage and contacting a licensed roofing contractor for a detailed estimate before calling your insurance company. Understanding your policy, especially the difference between RCV and ACV, is crucial for maximizing your payout and protecting your Palm Beach County home when you file a roof insurance claim Lake Park FL. Remember, timely submission of your roof insurance claim Lake Park FL can significantly impact the outcome.

Table of Contents

Important Considerations for Your Roof Insurance Claim Lake Park FL

Many homeowners in Lake Park, FL, have successfully navigated the roof insurance claim process by following best practices and seeking expert advice. Engaging with local roofing professionals will help ensure your roof insurance claim Lake Park FL is handled effectively.

- Step 1: Safely Assess and Document the Damage

- Step 2: Review Your Homeowner’s Insurance Policy

- Step 3: Get a Professional Roofing Estimate

- Step 4: File Your Claim Promptly

- Step 5: Meet with the Insurance Adjuster

- The BLU Roofing Advantage in Palm Beach County

- FAQ: Roof Insurance Claims in Lake Park

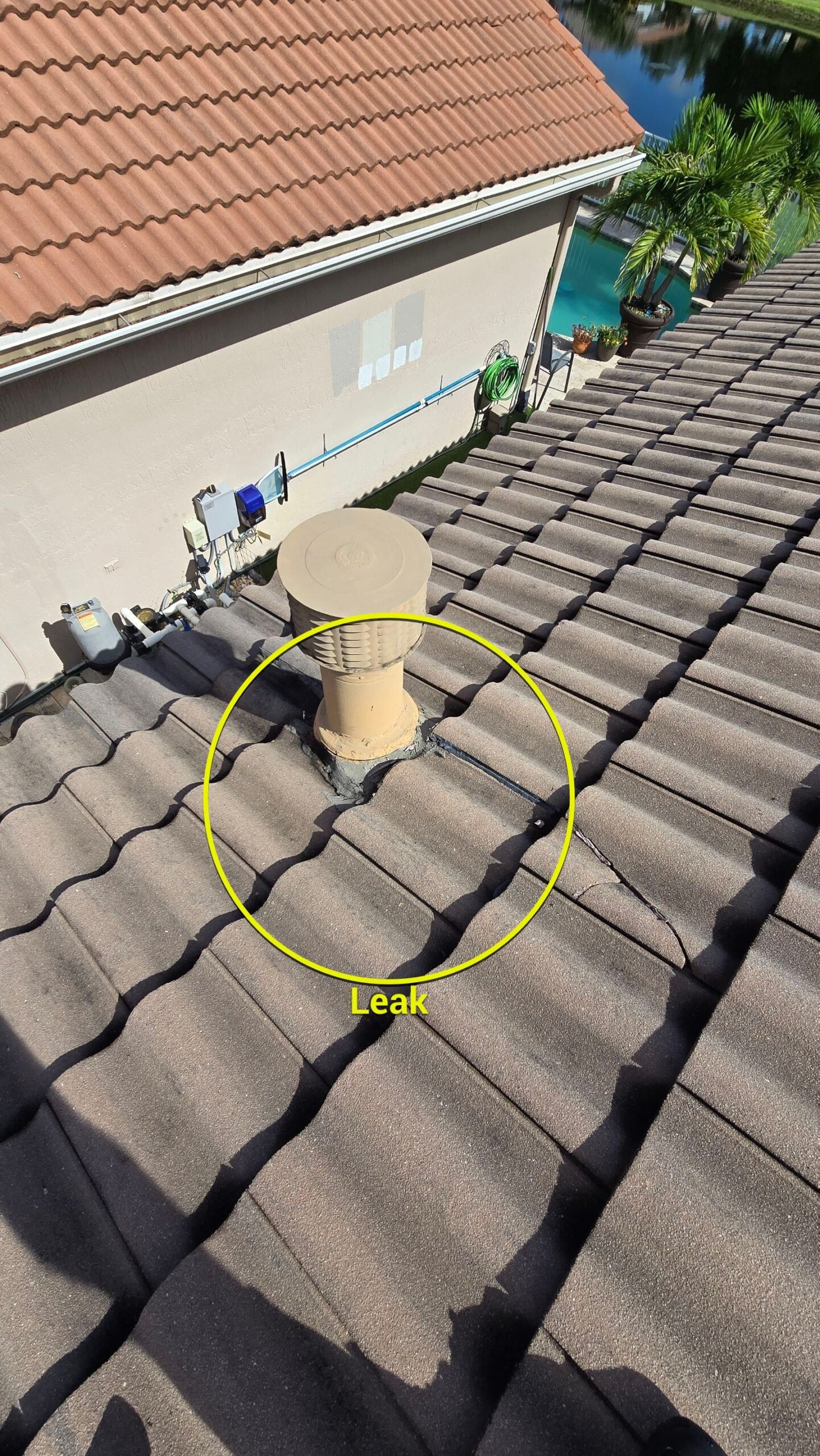

Step 1: Safely Assess and Document the Damage

After a severe storm passes through Palm Beach County, your first priority is safety. Do not climb onto your roof. Instead, perform a visual inspection from the ground using binoculars. Look for obvious signs of damage such as missing shingles, cracked tiles, or dented metal panels.

Inside your home, check your attic and ceilings for any signs of water intrusion or leaks. Document everything you see with clear, high-resolution photos and videos. This documentation will be vital when you file your claim.

Step 2: Review Your Homeowner’s Insurance Policy

Before contacting your insurance provider, take the time to review your policy. You need to understand your coverage limits, your deductible, and the specific perils covered.

Pay close attention to whether you have a Replacement Cost Value (RCV) or Actual Cash Value (ACV) policy. An RCV policy will cover the cost of a new roof without deducting for depreciation, while an ACV policy will only pay the current depreciated value of your old roof. Knowing this difference is essential for managing your expectations.

| Policy Type | What It Pays | Best For |

|---|---|---|

| Replacement Cost Value (RCV) | Full cost of a new roof, no depreciation deducted | Newer homes or newer roofs |

| Actual Cash Value (ACV) | Depreciated value of your old roof | Older homes, lower premiums |

Step 3: Get a Professional Roofing Estimate

This is perhaps the most critical step. Before the insurance adjuster arrives, you should have a detailed estimate from a reputable, licensed roofing contractor.

At BLU Roofing, we provide comprehensive inspections and detailed estimates that you can present to your insurance company. Having a professional assessment ensures that no damage is overlooked and provides a benchmark for the adjuster’s evaluation. If you need assistance, you can learn more about our residential roofing services or visit our specific Lake Park residential roofing page.

Step 4: File Your Claim Promptly

Once you have your documentation and a professional estimate, contact your insurance company to file the claim. Be prepared to provide the date and time of the storm, a description of the damage, and your photos.

Act quickly, as most insurance policies have strict time limits for filing claims after a storm event. Delaying could result in a denial of your claim. The Florida Department of Financial Services provides helpful guidance on your rights as a policyholder throughout this process.

Step 5: Meet with the Insurance Adjuster

Your insurance company will send an adjuster to inspect the damage. It is highly recommended that your roofing contractor be present during this inspection.

A professional roofer can point out specific damage that the adjuster might miss and advocate on your behalf to ensure a fair and accurate assessment. This collaborative approach often leads to a smoother claims process and a more favorable outcome for homeowners in Lake Park and neighboring cities like North Palm Beach and Palm Beach Gardens.

The BLU Roofing Advantage in Palm Beach County

Navigating a roof insurance claim can be daunting, but you don’t have to do it alone. By following these steps and partnering with a trusted local expert, you can ensure your home is fully restored. Based on our 2026 project data in Palm Beach County, homeowners who involve a professional contractor early in the process experience significantly fewer claim denials and faster resolution times.

FAQ: Roof Insurance Claims in Lake Park

Q: How long do I have to file a roof insurance claim in Florida?

A: In Florida, you typically have up to one year from the date of the storm or hurricane to file a claim. However, it is always best to file as soon as possible to prevent further damage and expedite the repair process.

Q: Will my insurance premium go up if I file a roof claim?

A: If the damage was caused by an “Act of God” such as a hurricane or severe storm, Florida law generally prohibits insurance companies from raising your premium based solely on that single claim. However, widespread storm damage in your area could lead to general rate increases for everyone.

Q: What if the insurance adjuster’s estimate is lower than my contractor’s estimate?

A: This is a common scenario. If there is a discrepancy, your contractor can review the adjuster’s estimate and provide a supplement detailing the missed items or underpriced materials. This is why having your contractor present during the adjuster’s inspection is so important.

Written By: Peter Menke

Peter Menke is the owner of BLU Roofing and has been serving the South Florida roofing industry for over 6 years. He founded BLU Roofing to provide homeowners with transparent, accurate data grounded in the reality of Florida’s unique climate and building codes, information that is often missing from generic national roofing advice. License #CCC1337285