Florida homeowners ask this more than almost any other roofing question, and for good reason. The state’s insurance market has been in turmoil for years, carriers have tightened their policies significantly, and the rules around what’s covered versus what isn’t are genuinely confusing. If you’re wondering whether homeowners insurance covers roof replacement in Florida, here’s a straight answer.

It Depends on the Cause of the Damage

Homeowners insurance in Florida is designed to cover sudden, accidental damage from specific covered perils — not the gradual deterioration that comes with age and normal wear. That distinction is the key to understanding what your policy will and won’t pay for.

What Is Typically Covered

Hurricane and windstorm damage is the most common covered cause in South Florida. If a named storm, tropical system, or severe windstorm damages your roof — missing tiles, torn underlayment, structural damage from wind pressure — your policy should cover the replacement cost minus your deductible. Florida policies typically carry a separate hurricane deductible calculated as a percentage of your home’s insured value rather than a flat dollar amount, so it can be significantly higher than your standard deductible.

Fallen trees and impact damage are also typically covered. If a tree falls on your roof, or flying debris during a storm causes direct impact damage, that generally qualifies as a covered loss.

Fire damage is covered under virtually all standard homeowners policies.

What Is Not Covered

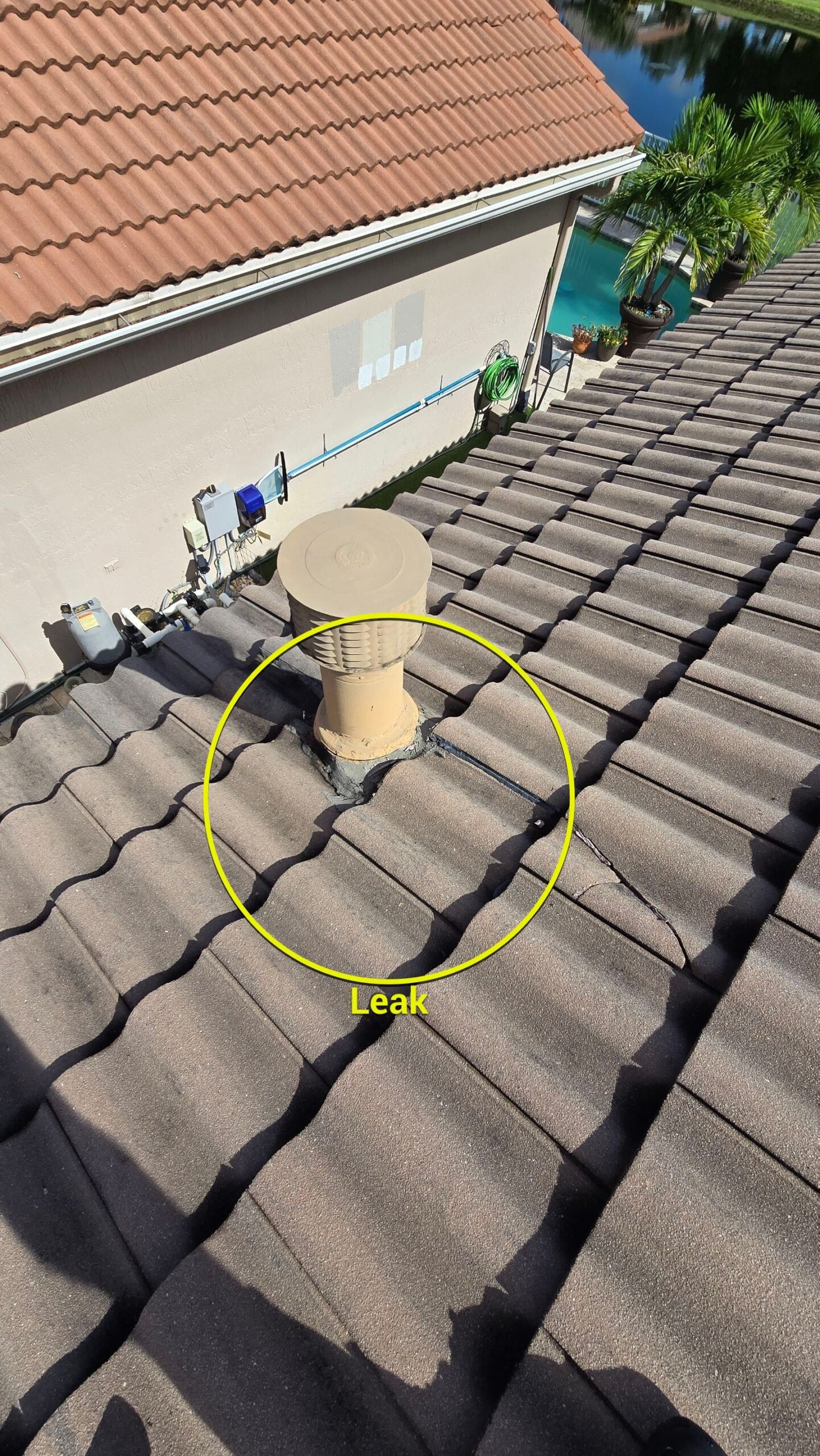

Normal wear and tear is not covered. If your roof has simply reached the end of its useful life — underlayment that has deteriorated over 20 years, tiles that have become brittle from UV exposure, or flashing that has corroded from salt air — that is considered a maintenance issue, not a covered loss. Insurance is not a home maintenance plan. If you’re unsure whether your roof’s condition is wear-and-tear or storm damage, a professional roof inspection can give you a clear, documented answer.

Pre-existing damage is not covered. If damage was present before your current policy was issued, or before a storm occurred, and you attempt to include it in a claim, that can result in claim denial and policy cancellation.

Neglect is not covered. If your roof leaked for years without being addressed and that deferred maintenance led to structural damage, your carrier can deny the claim outright. This is one of the most common reasons claims are denied in Palm Beach County — and one of the strongest arguments for getting ahead of problems early. Knowing the signs your roof needs immediate repair can protect both your home and your coverage.

What Florida Homeowners Need to Know Specifically

Roof age restrictions. Many Florida carriers now limit coverage on roofs older than 15 to 20 years, or will only pay actual cash value rather than replacement cost on older roofs. Some carriers won’t write or renew policies on homes in that age range at all. If your roof is approaching 15 years, review your policy language now — not after a storm. Understanding the cost of roof replacement in Palm Beach County ahead of time puts you in a much stronger position when that conversation with your insurer comes.

The 25 percent rule. Under the Florida Building Code, if more than 25 percent of your roof sustains damage, the entire roof or that section must be replaced rather than repaired. This rule can work in your favor during a claim. Damage that might otherwise be treated as a repair can cross that threshold and become a full replacement covered by your policy.

Carrier scrutiny is higher than it used to be. Florida has dealt with widespread fraudulent roofing claims over the past several years. As a result, insurers are more aggressive about reviewing and contesting claims than they were five years ago. The best protection against a disputed or underpaid claim is a licensed contractor who documents damage thoroughly, honestly, and in detail from the start.

How to Handle a Claim the Right Way

After any storm event, document the damage yourself with photos and video before anyone touches the roof. Then contact a licensed roofing contractor to assess the damage before your insurance adjuster visits. A knowledgeable contractor will identify damage that a non-roofing adjuster can miss and make sure the full scope of the loss is properly represented. Do not sign any document that assigns your insurance benefits to a third party without understanding exactly what you are signing.

Frequently Asked Questions

Do you help with insurance claims for storm damage?

Storms happen, and Florida insurance laws and claim procedures are always changing. If you believe your roof may have storm damage, BLU Roofing can inspect and document the condition of your roof. When insurance involvement is appropriate, we work alongside licensed public adjusters and insurance attorneys who can legally review your policy, consult on coverage, and assist with handling the insurance claim.

BLU Roofing Helps Palm Beach County Homeowners Through the Claims Process

We work alongside homeowners from the first inspection through the completed repair, making sure damage is properly documented and the scope of work is accurately represented to your carrier. If you’ve had storm damage or you’re not sure what your roof’s current condition means for your coverage, reach out for a free inspection and we’ll walk you through it.