As a homeowner in Boca Raton, dealing with roof damage, especially after a severe storm, can be a stressful experience. The process of filing a roof insurance claim can seem daunting, filled with paperwork, inspections, and negotiations. However, understanding the steps involved and knowing what to expect can significantly streamline the process and help ensure you receive the coverage you deserve. This 2026 guide is designed to walk Boca Raton residents through filing a successful roof insurance claim, minimizing delays and maximizing your claim payout.

Quick Summary

Filing a roof insurance claim in Boca Raton involves documenting damage, contacting your insurer, getting professional estimates, and negotiating for fair coverage. Act quickly after damage occurs, thoroughly document everything, and consider professional assistance to navigate the complexities of Florida insurance laws and ensure a successful claim.

Table of Contents

Act Quickly After Damage

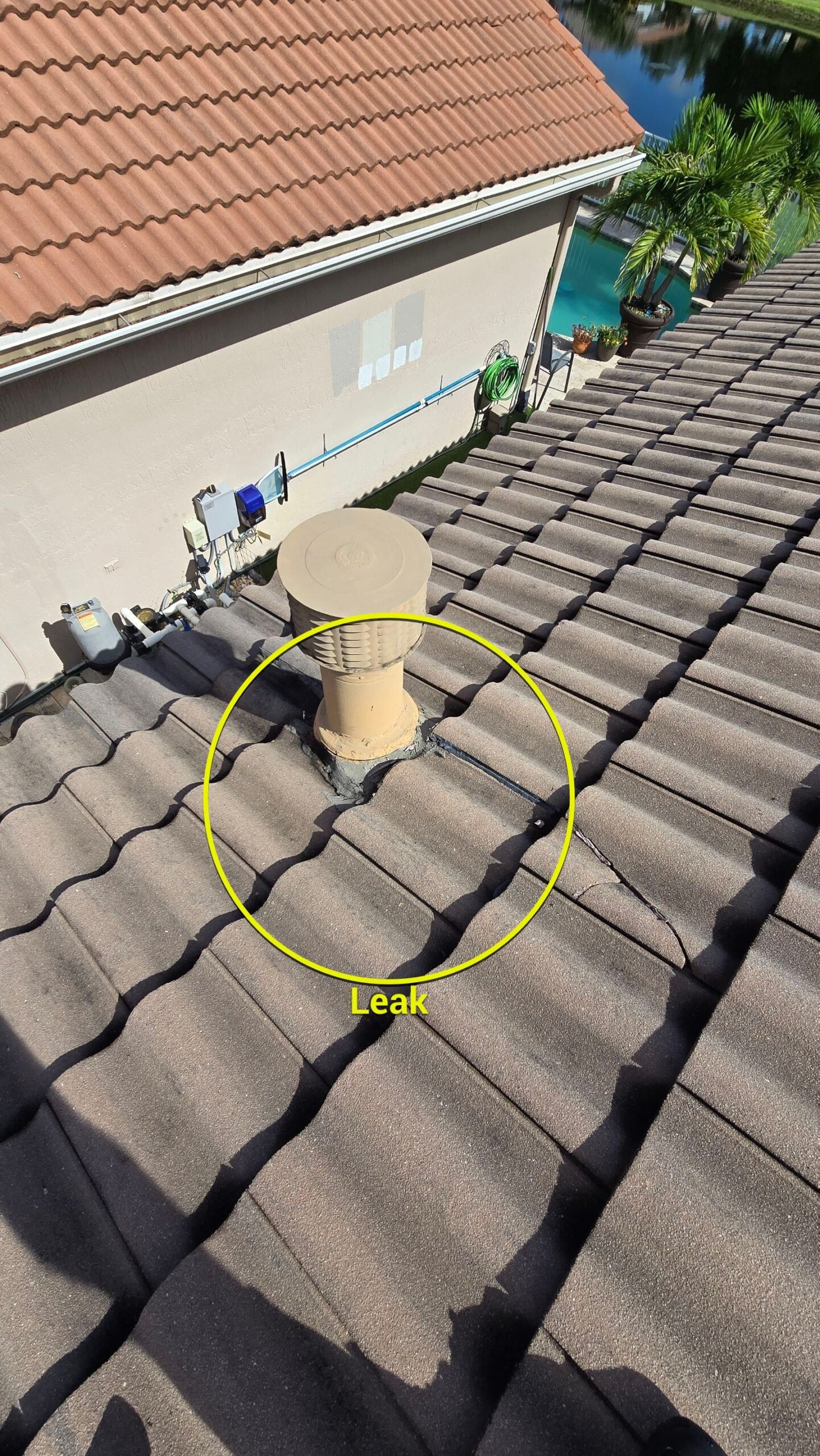

In Florida, insurance policies often have strict timelines for reporting damage. As soon as you notice any roof damage, especially after a hurricane or severe storm, it’s crucial to act promptly. Delaying notification to your insurance company could jeopardize your claim. Take immediate steps to prevent further damage, such as covering exposed areas with tarps, but avoid making permanent repairs until your insurer has assessed the damage. Remember, safety first, only assess damage from the ground if possible, or hire a professional to do so.

Understanding Your Policy

Before initiating a claim, thoroughly review your homeowner’s insurance policy. Pay close attention to sections regarding roof coverage, deductibles (especially hurricane deductibles), and depreciation. Many policies in Florida use Actual Cash Value (ACV) for older roofs, meaning they’ll pay for the depreciated value of your roof, not the cost of a new one. Replacement Cost Value (RCV) policies offer better coverage but are often more expensive. Understanding these terms will help you set realistic expectations and prepare for negotiations. For more details on Florida insurance laws, refer to the Florida Department of Financial Services.

Step-by-Step Guide to Filing a Claim

Filing a roof insurance claim can be broken down into several manageable steps. Here’s a checklist to guide Boca Raton homeowners through the process:

| Step | Action | Details & Tips |

|---|---|---|

| 1 | Document the Damage | Take clear photos and videos of all damage (interior and exterior) before any temporary repairs. Note dates and times. |

| 2 | Contact Your Insurer | Report the damage immediately. Provide all documentation. Get a claim number. |

| 3 | Temporary Repairs | Prevent further damage (e.g., tarping). Keep all receipts for reimbursement. Do NOT make permanent repairs yet. |

| 4 | Schedule Inspections | Your insurer will send an adjuster. Consider getting an independent roof inspection from a trusted contractor like BLU Roofing. |

| 5 | Review Estimates | Compare the adjuster’s estimate with your contractor’s. Ensure all damage is covered. |

| 6 | Negotiate & Settle | Be prepared to negotiate if the initial offer is too low. A reputable contractor can assist. |

| 7 | Roof Repair/Replacement | Once settled, proceed with repairs or roof replacement. Ensure all work is done to code. |

Common Challenges and How to Overcome Them

Filing an insurance claim isn’t always straightforward. Here are some common hurdles Boca Raton homeowners face and how to address them:

- Low Initial Offer: Insurers may offer less than the true cost of repairs. A detailed estimate from a trusted local roofing contractor is your best tool for negotiation.

- Denial of Claim: Claims can be denied for various reasons, such as pre-existing damage or insufficient documentation. Review the denial letter carefully and consider consulting with a public adjuster or attorney.

- Depreciation: If your policy is ACV, you’ll receive less for an older roof. Understand this upfront and be prepared for the difference.

- Contractor Scams: Be wary of contractors who solicit door-to-door after a storm, promising to handle your entire claim. Always choose a licensed, reputable local company like BLU Roofing.

BLU Roofing has extensive experience working with insurance companies in South Florida. We can provide accurate, detailed estimates and help you navigate the claims process to ensure your home is restored properly.

FAQ: Roof Insurance Claims

Q: How long do I have to file a roof insurance claim in Florida?

A: In Florida, the deadline to file a hurricane or windstorm claim is typically within two years from the date the damage occurred. However, it’s always best to report damage as soon as possible.

Q: What is the difference between ACV and RCV in roof insurance?

A: Actual Cash Value (ACV) pays for the depreciated value of your roof at the time of loss. Replacement Cost Value (RCV) pays for the cost to replace your roof with new materials of similar kind and quality, without deduction for depreciation.

Q: Should I get a contractor’s estimate before contacting my insurance company?

A: It’s highly recommended. A detailed estimate from a reputable roofing contractor provides crucial documentation and a benchmark for comparison when your insurance adjuster provides their assessment.

Q: What if my insurance company denies my roof claim?

A: If your claim is denied, request a detailed explanation in writing. You can then appeal the decision, provide additional documentation, or seek assistance from a public adjuster or an attorney specializing in insurance claims.

Written By: Peter Menke

Peter Menke is the owner of BLU Roofing and has been serving the South Florida roofing industry for over 6 years. He founded BLU Roofing to provide homeowners with transparent, accurate data grounded in the reality of Florida’s unique climate and building codes, information that is often missing from generic national roofing advice. License #CCC1337285