Filing a roof insurance claim in Florida is notoriously complex. Between recent legislative changes, aggressive insurance adjusters, and the sheer volume of claims after a major storm, homeowners in Palm Beach County often find themselves fighting for the coverage they pay for every month.

If your roof has suffered sudden, accidental damage from a hurricane, tropical storm, or severe wind event, you have the right to file a claim. Based on our 2026 project data in Palm Beach County, homeowners who follow a structured, documented process are significantly more likely to receive a fair settlement than those who rush the process.

Here is a step-by-step guide on how to file a roof insurance claim in Florida without getting your claim denied or underpaid.

Table of Contents

- Review Your Deductibles

- Document the Damage

- Get a Professional Inspection

- File the Claim

- Meet the Adjuster

- Review the Settlement

- FAQ

1. Review Your Deductibles

Before you call your insurance company, you need to know exactly what your policy covers and what your deductibles are. In Florida, most homeowners policies have two separate deductibles.

All Other Perils (AOP) Deductible: This applies to standard damage, like a tree falling on your roof during a typical thunderstorm. It is usually a flat dollar amount, such as $1,000 or $2,500.

Hurricane Deductible: This applies only when damage is caused by a named storm declared by the National Weather Service. It is typically a percentage of your home’s insured value, usually 2%, 5%, or 10%.

If your home in Jupiter is insured for $500,000 and you have a 5% hurricane deductible, you are responsible for the first $25,000 of damage before your insurance pays a dime. Knowing this number upfront helps you decide if filing a claim is even worth the potential premium increase.

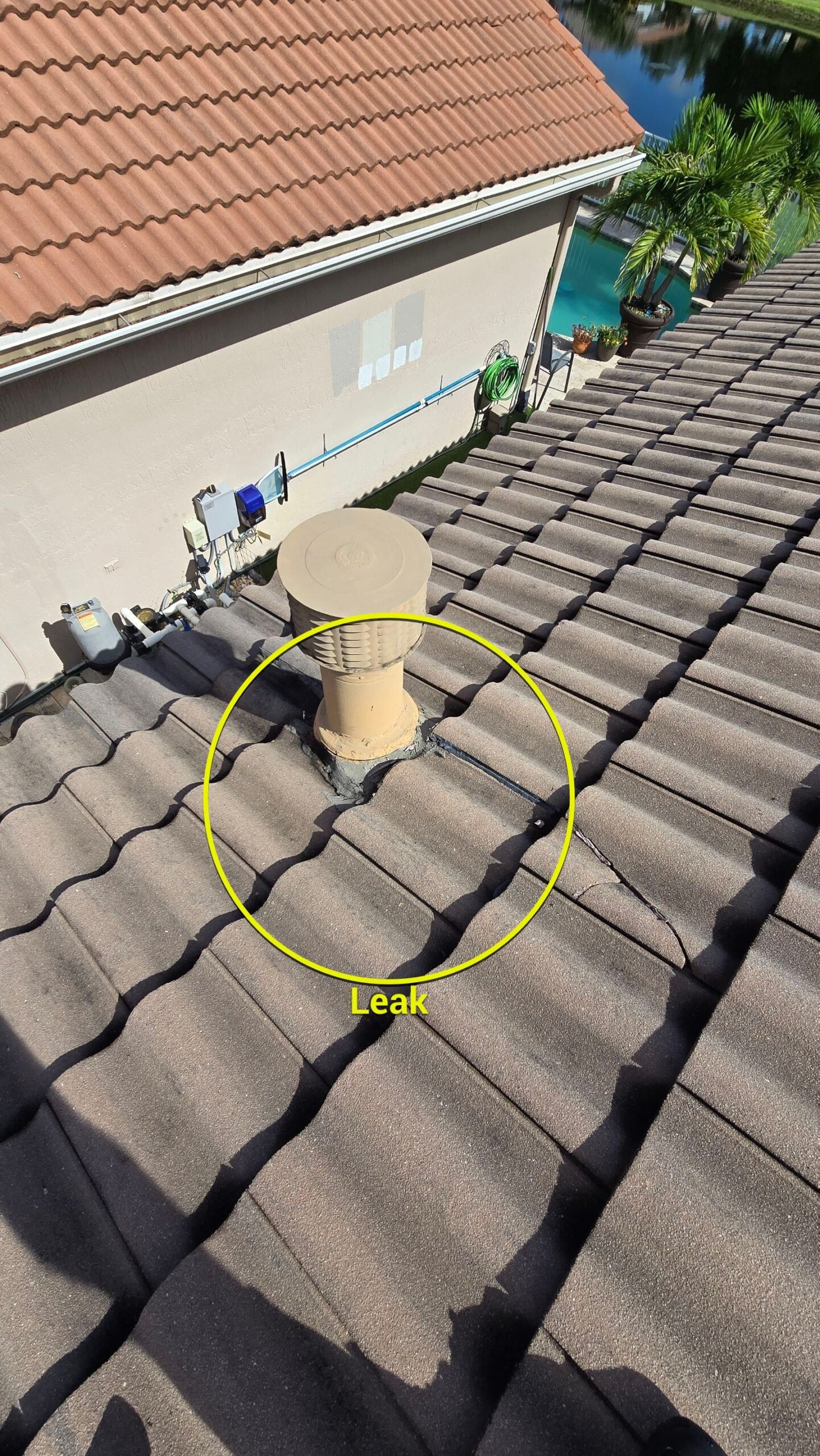

2. Document the Damage Immediately

Do not wait for an adjuster to arrive before documenting the damage. As soon as it is safe to do so, take extensive photos and videos of your property.

- Exterior: Photograph missing shingles, cracked tiles, dented metal panels, damaged flashing, and any debris that caused the damage. Take wide shots of the entire roof and close-ups of specific damage points.

- Interior: Photograph any water stains on ceilings or walls, bubbling paint, or active leaks. If water is entering your home, document the damage to your personal property.

- Mitigation: Florida law requires you to mitigate further damage. If you have an active leak, place buckets, move furniture, and lay down tarps. Photograph these mitigation efforts to prove you took reasonable steps to protect your property.

3. Get a Professional Inspection

Before you file the claim, get a professional assessment from a licensed, local roofing contractor in Palm Beach County.

An experienced roofer will inspect your roof, identify all storm-related damage, and provide a detailed, written estimate for the repairs or replacement. This estimate is critical evidence for your claim.

Warning: Do not sign an Assignment of Benefits (AoB) agreement with a roofing contractor at this stage. Recent Florida legislation has heavily restricted AoBs, but some contractors still attempt to use them. An AoB transfers your insurance claim rights to the contractor, giving them control over the process and the payout. A reputable contractor will provide an estimate without requiring an AoB.

4. File the Claim with Your Insurance Company

Once you have your documentation and a contractor’s estimate, contact your insurance company to formally file the claim.

Be prepared to provide your policy number, the date and time the damage occurred, a detailed description of the damage, the photos and videos you took, and the roofing contractor’s estimate. Your insurance company will assign a claim number and an adjuster to your case.

5. Meet with the Insurance Adjuster

The insurance company will send an adjuster to inspect your roof and assess the damage. It is highly recommended that your roofing contractor is present during this inspection.

The adjuster works for the insurance company; their goal is to minimize the payout. Your roofing contractor works for you; their goal is to ensure all damage is identified and properly accounted for in the estimate. Having your contractor present ensures the adjuster sees the full scope of the damage, especially in complex systems like concrete tile or standing seam metal roofs.

6. Review the Settlement Offer

After the inspection, the adjuster will provide an estimate of the damages and a settlement offer. Compare this offer carefully against your roofing contractor’s estimate.

If the insurance company’s offer is significantly lower than your contractor’s estimate, do not accept it immediately. You have the right to dispute the offer. Your contractor can provide additional documentation, photos, or Florida Building Code requirements to justify their estimate and negotiate with the adjuster on your behalf.

Once you and the insurance company agree on a settlement amount, you will typically receive an initial payment representing the Actual Cash Value of your roof minus your deductible. You can then authorize your roofing contractor to begin the repairs or replacement. Once the work is completed and passes the final county inspection, your contractor will submit a final invoice to the insurance company, which will then release the remaining funds to cover the full cost of the project.

For more information on what to expect during the replacement process, see our Palm Beach County homeowner’s guide to roof replacement.

Frequently Asked Questions

How long do I have to file a roof insurance claim in Florida?

Under recent Florida law changes, you generally have one year from the date of the storm or hurricane to file a new or reopened claim, and 18 months to file a supplemental claim. However, it is always best to file as soon as possible after the damage occurs.

Will my insurance company drop me if I file a roof claim?

Florida law prohibits insurance companies from canceling or non-renewing a policy solely because you filed a claim for an Act of God, such as a hurricane or severe storm. However, they can choose not to renew your policy for other reasons, such as the age of your roof.

Does insurance cover the cost of bringing my roof up to current building codes?

If you have “Ordinance or Law” coverage in your policy, your insurance will cover the additional costs required to bring your new roof up to the current Florida Building Code standards. This is crucial in South Florida, where building codes are frequently updated for hurricane resilience.

Written By: Peter Menke

Peter Menke is the owner of BLU Roofing and has been serving the South Florida roofing industry for over 6 years. He founded BLU Roofing to provide homeowners with transparent, accurate data grounded in the reality of Florida’s unique climate and building codes, information that is often missing from generic national roofing advice.